Let’s face it — Medicare is complicated. Between the terms for Medicare eligibility, the multiple Medicare coverage options, and the new changes concerning Medicare insurance cards, understanding all the healthcare options can be difficult. It can be even harder to explain healthcare options to new hires, residents, and resident family members.

The good news is that we’ve put in the leg-work for you! We’ve outlined the most important information in this Medicare Training 101 guide and specifically geared it toward senior care administrators. Whether you’re using this to refresh yourself on Medicare basics or teach others about Medicare, it’s sure to be a helpful resource to have in your administrative tool-belt.

Medicare Basics

What Is Medicare?

Medicare is a health insurance program that’s federally funded and intended for certain individuals who meet the requirements. The program is made up of various segments that cover most expenses such as hospital stays, medical services, and prescription drugs.

Who Is Eligible for Medicare?

Medicare was originally created for individuals who are 65 years old or older. However, Medicare can also be provided to younger individuals with disabilities and those who have End-Stage Renal Disease (ESRD).

Individuals can enroll in Medicare by going to SocialSecurity.gov, calling the Social Security office, or visiting a local Social Security office in person. In some instances, people may be automatically enrolled in Medicare, so it’s important to check the stipulations. The Medicare open enrollment period begins three months before an individual turns 65. It ends three months after their birthday month (a total of seven months).

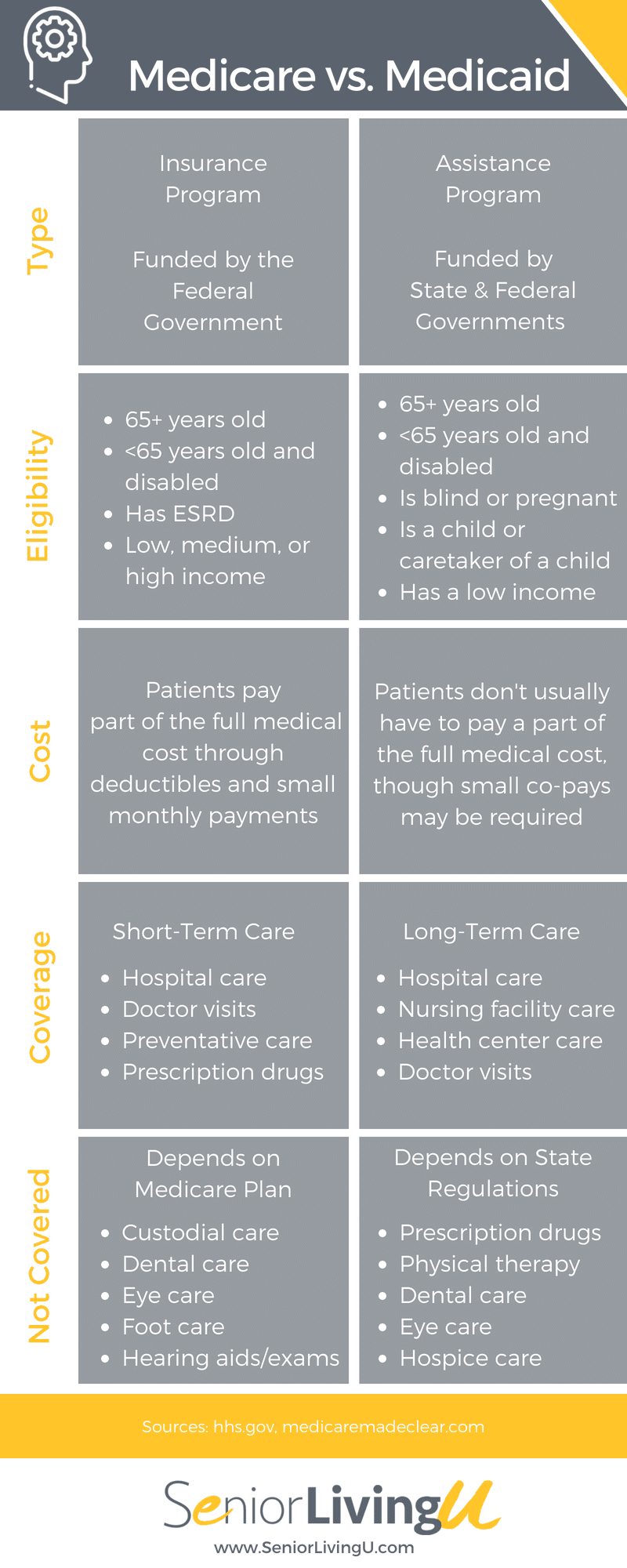

Medicare vs. Medicaid

“What’s the difference between Medicare and Medicaid?” It’s a common question when it comes to health insurance. Take a look at our infographic to easily compare and contrast Medicare and Medicaid features.

Can Someone Have Both Medicare and Medicaid?

Yes, they can! A person is deemed “dual eligible” when they qualify for both Medicare and Medicaid. If they are dual eligible, most of their healthcare costs will be paid for and any premiums required for Medicare will be minimal.

How Does Dual Eligibility Help Seniors?

If a senior is eligible for both Medicare and Medicaid, they’ll benefit by having to pay very little (or nothing at all) for their medical services. This is great, especially for retired seniors or seniors in assisted living facilities that have minimal income. Medicare will provide coverage for things such as hospital care, doctor visits, preventative care, and prescription drugs, and Medicaid will fill in the gaps by paying for things like Medicare premiums, additional medical services, and out-of-pocket expenses.

Medicare Coverage Choices

Deciding on a type of Medicare coverage can be tricky. To help, we’ve separated each Medicare segment so you can easily distinguish them from one another.

What Does Medicare Part A Cover?

This Medicare segment is also called “Original Medicare” and “Hospital Insurance.” It primarily covers inpatient hospital care, short-term nursing home rehabilitative care, hospice care, and short-term home health services. This is the “free” part of Medicare that an individual should get if they worked for more than ten years.

What Does Medicare Part B Cover?

Medicare Part B is the second segment of “Original Medicare” and is also known as “Medical Insurance.” It provides coverage for medically-necessary services and supplies needed to diagnose or treat medical conditions. This includes lab services, durable medical equipment (DME), preventative care, surgical fees, and outpatient physical therapy. Plan B is paid for by a monthly deduction from Social Security payments.

What Does Medicare Part C Cover?

Also known as Medicare Advantage (MA) Plans, Medicare Part C is offered by private companies that have collaborated with Medicare. Medicare Advantage Plans can be thought of as this:

Part C = Part A + Part B + Part D (Sometimes)

Medicare Advantage Plans provide the same benefits as Part A and Part B, and can even include Medicare Part D for prescription drug coverage. Medicare Advantage Plans are usually offered as:

- Health Maintenance Organizations (HMO) Plans

- Preferred Provider Organizations (PPO) Plans

- Private Fee-for-Service (PFFS) Plans

- Special Needs (SNP) Plans

What Does Medicare Part D Cover?

Medicare Part D, also called the “Medicare Drug Plan,” provides prescription drug coverage and can be added to other Medicare plans. This segment can help lower prescription drug costs and protect against individual costs increasing in the future.

Which Medicare Plan Should I Choose?

Medicare plans should be chosen based on an individual and their family’s specific needs. To figure out if an item, test, or service is covered by any of the plans, use the Medicare search tool to find it.

If an individual only has Part A and B, they may want to consider integrating a Medicare Supplement (Medigap) Plan to help pay for the services and additional expenses that aren’t covered. Medigap Plans are used in conjunction with Original Medicare Plans to cover leftover costs that people would have to pay out-of-pocket otherwise. These costs would include:

- Part A coinsurance and hospital costs up to a year after Medicare benefits are used up

- Part A hospice care coinsurance or copayments

- Part B coinsurance or copayments

While Medicare Advantage Plans (Part C) often look like an attractive alternative to Medicare Parts A and B with a Medigap Supplement, they have pros and cons just like any other insurance choice. Part C plans are great because they are often more affordable and include drug, dental, vision, hearing aid, and fitness benefits. The downfall is that Part C recipients are limited to a restricted list of doctors and skilled nursing home rehabilitation centers. Due to the restrictions, some individuals may receive shortened therapy or skilled nursing care.

How Is Medicare Changing?

A new law is requiring the Centers for Medicare & Medicaid Services (CMS) to update all Medicare cards by April 2019. They will be removing all Social Security Numbers (SSNs) and Health Insurance Claim Numbers (HICNs) from the cards and replacing them with Medicare Beneficiary Identifiers (MBIs). This is to help decrease identity theft and illegal use of Medicare benefits.

What Do Senior Living Facilities Need to Be Aware Of?

All facility systems should have been updated to accept the new MBIs by April 2018 to ensure easy billing and filing of claims. During the transition period from April 1, 2018 to December 31, 2019, healthcare establishments will be allowed to accept either the new MBI or the old HICN. At the beginning of 2020, only the MBI will be accepted unless individuals are filing an appeal, checking the status of a claim, or searching for a claim that began prior to December 31, 2019.

Is this online course for administrator only?

I am a CHPNA, Hospice Liaison and would like to find a certificate course on medicare/medicaid.

I am in the State of Maine if you are unable to help me perhaps you could guide me in the right direction.

Thanks.